|

Summary

My previous candidates for a takeout were Intercept Pharmaceuticals (NASDAQ:ICPT), Progenics Pharmaceuticals (NASDAQ:PGNX), and Anthera Pharmaceuticals (NASDAQ:ANTH). The former has a market cap of around $4.5 billion, while the latter two have market caps of less than $500 million. All three have enormous potential but may not be worth Gilead's dime. Acquiring a company of greater magnitude would open many, more lucrative doors to Gilead. In my opinion, Gilead does not need to roll the dice and acquire companies whose success largely lies in Phase III drugs -- such as the ones listed above -- when it can overtake an established company with many drugs in its pipeline and already on the market. Gilead's Q3 earnings report told investors that the company is sitting on $25.1 in cash and cash equivalents (up from $14.7 billion in Q2 largely due to the issuance of $10 billion in senior unsecured notes in September). To me, the large-cap name that makes the most sense is Bristol-Myers Squibb (NYSE:BMY). I believe the potential synergies make this deal attractive to both companies, and Gilead has the capacity to make an enticing offer. Before I discuss why it should be Bristol-Myers, allow me to explain why it is so important that Gilead pulls the trigger at all. We know that the company has the cash to support a deal. That's the can aspect. Theneed component is completely different animal. Gilead is almost entirely dependent on its HCV pipeline for its revenue and earnings. More than 90% of Gilead's 2014 product sales came from its HCV drugs. Specifically, about 41% of revenue came from Gilead's HCV darling Sovaldi. While this is sustainable in the present and near future, this may not be the case for long. There are worries of slowing Hepatitis C prescription growth, and investors worry that Merck's (NYSE:MRK) entry into the Hepatitis C market in early 2016 will take market share from Gilead. To ensure stability in the future, Gilead needs to diversify now. This is what Bristol-Myers brings to the table. The company has a large and well diversified product line, with products beginning with virtually every letter of the alphabet and treating schizophrenia, bipolar disorder, and depression to melanoma. In its pipeline, there are over 20 drugs in phase I, six in Phase II, and four in Phase III. Gilead has eight Phase I drugs, 16 in Phase II, and nine in Phase III. Of course, most of the drugs in Phases I & II will not make it to market, but the high amount of Phase I drugs that Bristol-Myers brings to the table could be key to unlocking years of a diversified pipeline. Like I said: if Gilead wants to ensure stability in the future, it must diversify now.

Zoom in on Bristol-Myers' pipeline, and you'll see that the company has a strong presence in the oncology and immuno-oncology markets. Immuno-oncology is an innovative form of cancer treatment. This area of research seeks to help the body's immune system fight cancer, rather than removing it or treating it with chemotherapy. Bristol-Myers' website has a great analogy that contrasts immuno-oncology with other forms of cancer treatment. For patients with advanced cancers and ones that have spread throughout the body, immuno-oncology can be the solution to these hard-to-treat problems.

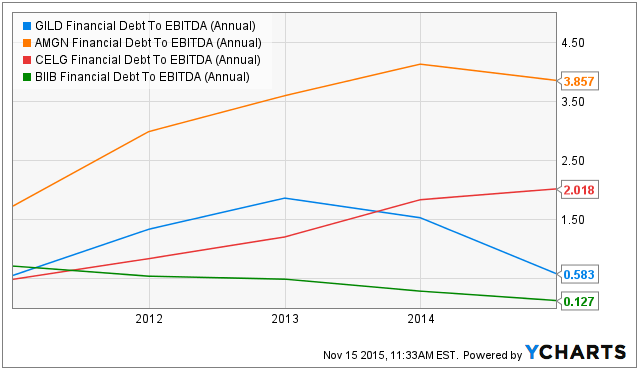

The immuno-oncology market is predicted, by Leerink Partners analysts, to be a $40 billion market ten years from now. This fact is not unknown to John Martin, CEO of Gilead, whose company has no current exposure to immuno-oncology; eventually, Gilead will make its way into this segment of the market. However, taking over Bristol-Myers would give Gilead immediate entry into the immuno-oncology space, allowing the combined company to become the leader. The $113 billion company is currently conducting clinical trials for immuno-oncology on the following cancer types: cervical cancer, colorectal, gastric cancer, glioblastoma, head and neck cancer, kidney cancer, leukemia, liver cancer, lung cancer, lymphoma, melanoma, multiple myeloma, ovarian, and prostate cancer. Though unfortunate, it is clear that the applications of immuno-oncology are very extensive. Bristol-Myers' market cap would obviously make it impossible for Gilead to complete a takeover in an all-cash deal. From Gilead's last major acquisition, Pharmasset, investors know that Gilead has no problem using a combination of debt, cash, and senior unsecured notes to make a deal happen. As stated earlier, Gilead raised $10 billion in September from issuing senior unsecured notes. I've read countless articles that believe Gilead is tipping its hand in doing this, but I don't think that the issuance of these notes, in and of itself, means an acquisition is right around the corner. What I do think this means, though, is that Gilead is gearing up to make an acquisition of a larger scale, and is forgetting the Intercepts of the biopharmaceutical world. Now that the compelling synergies have been discussed, let's ask the 64,000 question: Can Gilead even afford to buy Bristol-Myers? In short, yes. Gilead's current financial debt to EBITDA (earnings before interest, tax, depreciation, and amortization) ratio stands at 0.583. This is second only to Biogen (NASDAQ:BIIB).

GILD, CELG, BIIB, AMGN Financial Debt To EBITDA (Annual) data by YCharts

This multiple is derived by dividing Gilead's $12.3 in financial debt by its full year 2016 EBITDA estimate of roughly $21.1 billion. A ratio close to 2 is considered a risky investment, while a ratio under 1 shows that the company is in good financial standing. But we must keep in mind that we are talking about the biotech sector which, by nature of the deals that take place, requires the use of a debt far more often than that of cash. A lot of risk is already priced into biotech stocks for investors know of this reality. When this reality is coupled with Gilead's free cash flow, I believe that it is extremely reasonable to assign the company a 4.5x financial debt to EBITDA multiple. (To me, a 3x multiple for a company in the biotech sector is more down to earth, but I believe that Gilead deserves a premium due to its incredible cash flow). Multiplying $21.1 billion by 4.5 brings me to $94.95 billion. Throw in cash and the senior unsecured notes, and Gilead could raise about than $120 billion to acquire Bristol-Myers. After the recent bear market that tore through the biotech sector, Bristol-Myers has come off its highs (though not as much as other stocks). I believe that Gilead may have missed its chance to strike, but that there is still a case to be made based on valuation. Bristol-Myers trades 35.5x this year's earnings, which is a lofty premium to the market. Gilead would, of course, have to offer a premium on top of this to reward BMY shareholders, but I do not think it would be one that would cause the stock to pop, say, 86%, like Pharmasset did on the day that it was acquired. I think that at just 9x earnings there is a strong case to be long Gilead. GILD is an incredibly inexpensive stock that has a world of opportunity and pays you to wait -- via a 1.61% yield -- for an acquisition. The stock has substantially come off of its highs, and I think that the acquisition of a large-cap company would make this name an investor-favorite once again.

0 Comments

Leave a Reply. |